We have repeatedly written about the need to play defensively when investing. Playing defensively means to first avoid costly mistakes rather than trying to hit winners. Amongst the first steps to avoiding costly mistakes is minimizing intermediary expenses and reducing tax drag on investments. Distributor/agent commissions, brokerage and investment advisory fees are vital ingredients of intermediary expenses. Keeping these to a minimum has a significant impact on the long term healthy growth of investments. Every investor must do her homework and understand how much commissions, brokerage and investment advisory fees she is spending on an annual basis. Investment advisory fees is transparent and obvious to the investor, since the investor herself writes a cheque/makes an online transfer to the investment adviser against the invoiced amount for advisory services offered. Commissions on the other hand are more difficult to unearth – since the investor is unaware of commissions being paid from her pocket (investments) to the distributor. Sometimes investors are even unaware of who is the distributor !! The title of this blog urges, you the investor to do your homework and make yourself aware of what is sometimes unbeknownst to you going out of your own pocket.

SEBI issued a circular SEBI/HO/IMD/DF2/CIR/P/2016/42 on 18-Mar-2016 regarding certain additional disclosures to be made in the half yearly Consolidated Account Statement (CAS) issued to investors. Amongst the salient points of the circular, point A(2)(a) mandates mutual funds to disclose the actual commissions paid by mutual funds to distributors during the half year period. The exact words are as follows :

Further, CAS issued for the half-year(September/ March) shall also provide:

a. The amount of actual commission paid by AMCs/Mutual Funds (MFs) to distributors (in absolute terms) during the half-year period against the concerned investor’s total investments in each MF scheme. The term ‘commission’ here refers to all direct monetary payments and other payments made in the form of gifts / rewards, trips, event sponsorships etc. by AMCs/MFs to distributors.

Searching in the maze:

The CAS (Consolidated Account Statement) is issued by NSDL or CDSL, the two SEBI registered depositories in India. Investors receive this CAS through email on a monthly basis, however only the CAS with dates of 30-Sep and 31-Mar (half-year) are required to report the commissions paid to mutual fund distributors. Further each CAS has multiple sections. Sifting through this maze of information is an effort in itself. It is quite easy to miss out on the vital section containing the commissions paid out by investors. For ease the following are the steps for checking the eCAS from NSDL:

Step 1:

Locate your eCAS statement of date 31-Mar or 30-Sep. Only the statements of 31-Mar and 30-Sep will have this information. There is no point in opening a CAS of any other date.

Step 2 :

Open the eCAS with the appropriate password (It is your PAN in caps for NSDL eCAS).

Step 3 :

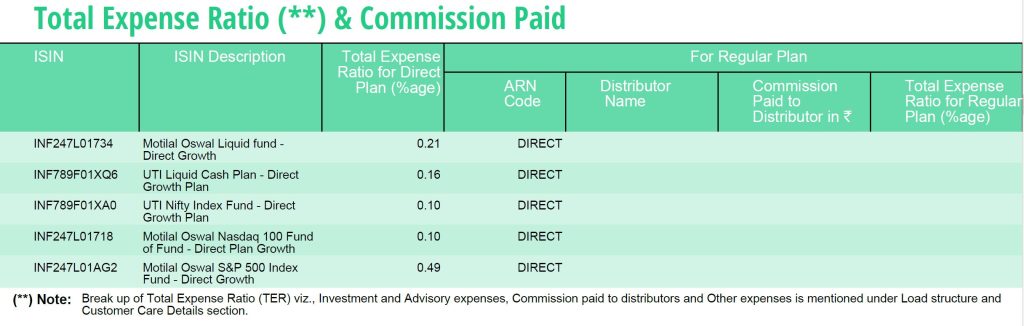

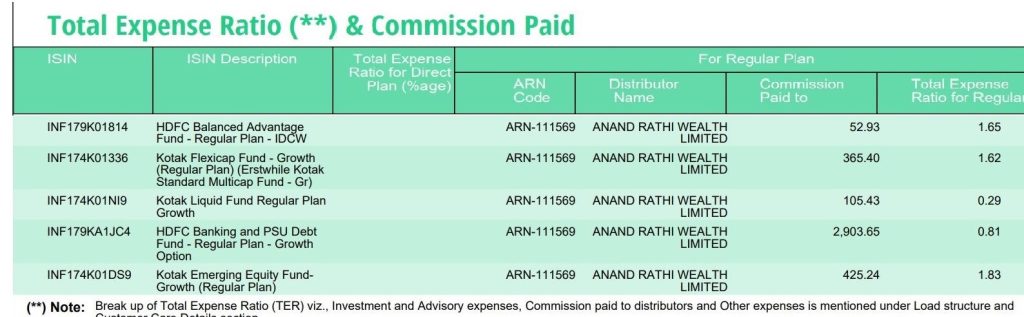

Scroll down to the bottom of the Holdings section. Towards the end of the section, just before the Transactions section. There will be a green table with title Total Expense Ratio (**) & Commission Paid . Alternately you can go to the search icon (magnifying glass) in adobe and search for the word Commission . The table looks like this :

The table above indicates the absolute amount paid to the distributor during the half year period of interest. If you multiply these numbers by two you will get an indicative idea of how much you are paying your distributor annually. If you divide the amount you are paying your distributor annually by the total value of your mutual funds you will understand how much you are paying your distributor as a percentage of the funds that are invested. Do note that the commissions paid for Structured Products and Portfolio Managed Services is not reported here. Ofcourse commissions paid on insurance products is also NOT reported here. Nevertheless for mutual funds atleast you are now aware how much you are paying your mutual fund distribitor. As an exercise, I urge you to comb through your investments and establish how much commissions you are annually paying in total. Do this for your mutual funds (as discussed), your Insurance products, your Portfolio Managed Services and your Structured Products. Rationalizing commissions can save you a bundle. A similar commissions table is presented below, where all mutual funds are purchased in the DIRECT mode. You will note that no commissions are paid out and no distributor exists – all investments are DIRECT.