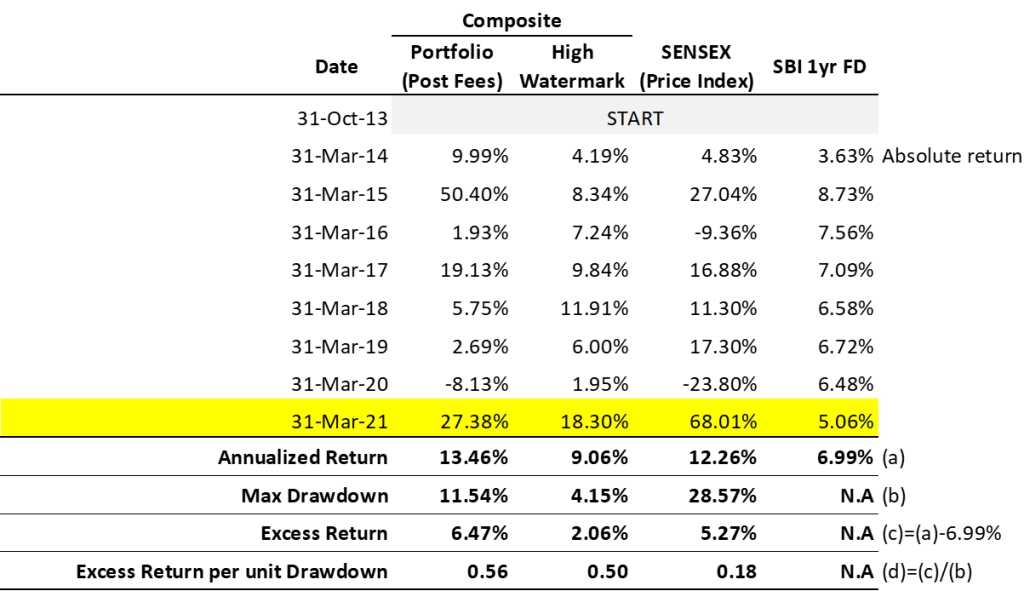

Our composite portfolio is the sum total of all individual client portfolio values and our composite high water mark is the sum total of all individual client high water marks. The performance being reported in this annual report is a time weighted return (TWRR) as against the cash weighted XIRR being reported in each of your individual portfolios. There is a distinction between the two – the subject upon which we have written a blog. Aroha’s (unaudited) performance on a composite level is reported in the table below :

In the concluding statement of our report card dated 31-Mar-20, we had said :

“We remain convinced that economic activity is bound to come back. There remains NO OTHER OPTION for a young country such as ours. If you as an investor also believe so – then there is no better time to invest incremental risk capital in companies with sound business models in a steady drip over the next three months. Thank you for one more year of trust.”

Clients who added additional capital at the depths of last year’s mayhem or those for whom we redeployed liquid fund positions into equity have benefited handsomely on an absolute basis. After a four year hiatus, Aroha has this year outperformed the composite highwater mark. Since inception, over an eight year period Aroha’s composite portfolio has generated a TWRR of 13.46% versus 9.06% for the composite highwater mark. This outperformance in return when normalized for maximum drawdowns shows that the excess return per unit drawdown is 0.56 for the composite portfolio versus 0.50 for the composite high water mark. Though better, 0.56 is not very different from 0.50 – and this indicates that most of the outperformance in return has been obtained due to higher risk rather than true alpha generation. This stands in sharp contrast to last year, wherein the corresponding numbers on 31-Mar-20 were 0.36 for the composite portfolio versus 0.09 for the composite highwater mark. Aroha’s higher return on 31-Mar-20, even when adjusted for max drawdown, indicated a significant alpha (outperformance). This dramatic change from 31-Mar-20 to 31-Mar-21 is a result of the rapid run up in eqity markets over the last one year. In times of market stress our composite portfolio tends to significantly outperform on a risk adjusted basis.

Active portfolios while having performed well on an absolute basis, have in-fact under-performed the benchmarks. The rapidity with which the markets have turned the corner has surprised us all. It is in our mind a prudent time to make a close examination of the risks in client portfolios now and re-allocate if necessary as per original Investment Policy mandates.

Thank you dear clients for your continuing trust.